Personal Loan Types and Terms

Common Types of Personal Loans

When you need access to cash, there are a number of personal loan products available to borrowers. Common types of personal loans include secured, unsecured, fixed- rate, variable-rate and debt consolidation loans. If you’re interested in securing a personal loan, it just makes good sense to understand the personal loan landscape before taking action.

Choosing the right financial instrument depends on your unique life circumstances and financial position. Perhaps you’re already familiar with the most common types of personal loans, but the following information may prove useful as you consider the available personal loan products.

- Secured loans

- Personal Loans

- Unsecured loans

- Fixed-rate personal loans

- Variable-rate personal loans

- Debt consolidation loans

- Personal lines of credit

- Personal loans that require a co-signer

- Other types of loans that may be offered by lenders

Unsecured Personal Loans

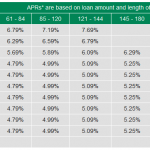

The majority of personal loans are unsecured. This means that you’ll have to make fixed payments, but you won’t have to provide collateral to qualify for a loan. Your ability to qualify for an unsecured loan will depend on your credit score and the length of time you need to pay off the loan. An unsecured personal loan carries a greater level of risk for lenders. The loan is based solely on your personal credit history and ability to repay the loan. If you default on the loan, the lender doesn’t have the option of selling collateral such as a home or vehicle. Creditors usually charge a higher rate of interest on unsecured loans to make up for the lack of colateral. Monitor your credit score and challenge any inaccurate information to maximize your credit rating.

Depending on your credit score, you can expect to pay anywhere from 5 to 36 percent interest on an unsecured personal loan. Check with lenders to determine the rate of interest and repayment plans that are available. Once your unsecured loan is approved, and depending on your credit worthiness and loan amount, you will be given one to seven years to repay the loan. Lender loan rates and terms vary, so take the time to research the options that are available to you.

Secured Loans

Secured Loans

Secured personal loans are tied to some sort of collateral. The lender has the legal right to seize the collateral if you fail to meet your payment obligations. Defaulting on a collateralized loan will be reflected in your credit rating. Common types of personal loans secured by collateral are car loans and home mortgages. Secured loans are provided by many credit unions, banks and various online lenders. Secured loan interest rates are a bit lower than for unsecured loans, but comprehensive research is still recommended.

Fixed-Rate Personal Loans

In most cases, personal loan payments are based on a fixed rate of interest. This means that your monthly payments will remain constant until you have fulfilled your payment obligations. Aside from consistent payments, a fixed-rate loan also provides protection against rising interest rates and higher payments.

Variable-Rate Personal Loans

The rate of interest on a variable-rate loan fluctuates in accordance with the current benchmark rate of interest established by banks. This means that you could benefit from lower payments during a season of falling interest rates, but you also face the risk of incurring higher interest rates and monthly payments. Variable rate loans are attractive because they usually carry a lower rate of interest than fixed-rate loans.

You should be aware of any interest rate caps that are included in the loan contract. An interest rate cap limits how often and how much a lender can increase the rate of interest on your personal loan. Keep in mind that the level of risk associated with variable-rate loans diminishes when you choose shorter repayment terms.

Debt Consolidation Loans

Debt Consolidation Loans

You may be able to save on your monthly expenses by consolidating multiple debts into a single personal loan. This option may make you eligible for a lower rate of interest and reduced total monthly payments.

Lines of Credit

If you qualify for a personal line of credit, you’ll have access to an established amount of revolving credit at a specified rate of interest. It works pretty much like a credit card. You can access any remaining portion of your standing credit line whenever the need arises. You only pay interest on the amount you actually borrow. The remainder of your credit limit will be ready if you need the money for an unexpected emergency or other expenses.

Although a personal line of credit isn’t ideal for funding a one-time expense, it can be useful for relieving imbalances in income and paying for unplanned expenses. The key is to pay down the line of credit when income is at normal levels. The combination of a maxed-out credit line and the onset of higher than usual expenses can be problematic.

Personal Loans That Require a Co-Signer

If you have little or no credit, a co-signer may put you on the road to a higher credit score and access to future loans. If you can find a willing co-signer, why not piggyback on the credit worthiness of a friend or relative to begin building your financial future. When a co-signer promises to repay your personal loan if you are unable to meet your payment obligations, you will receive all the benefits of the co-signer’s established credit history. Relying on a co-signer also provides you with an opportunity to build your own credit history.

Other Kinds of Personal Loans

Pawnshop Loans

If you own something of value, a pawnshop will give you a secured loan. The amount of the loan will depend on the value of the asset you exchange for a cash loan. Common types of collateral used for a pawnshop loan include musical instruments, electronic devices and jewelry. The pawnshop will take possession of your collateral and give you a certain amount of time to repay the loan with interest. The pawnshop has the right to sell your property if you fail to repay the loan within a prescribed period of time. The interest on pawnshop loans is high, but your credit score will be unaffected if you decide not to repay the loan and lose your collateral.

Payday Loans

A payday loan is an unsecured loan that usually has to be repaid in full when the borrower receives their next paycheck. You might be able to borrow a few hundred dollars at a relatively high rate of interest. Many borrowers end up taking out additional loans when they are unable to repay their initial payday loan. Payday loans are risky and often result in a debt trap that includes triple digit interest charges.

Credit Card Cash Advance

Most credit cards allow you to access a prescribed amount of cash. Using your credit card to secure a short-term loan with the assistance of an ATM or bank generally results in high interest rate charges, special fees and higher credit card payments.

{kind=link}