Title Loan Statistics

Auto Title Loan Facts 2019

Auto title loans are a method to get money when needed. These short-term loans are provided by using a vehicle as collateral. The loans are often available in an amount up to the value of the vehicle being used as collateral. The lender often retains the title of the vehicle throughout the duration of the loan. These loans are often attractive to those with poor credit who are unable to receive a traditional loan. Before seeking an auto title loan, these top 9 facts should be considered.

- Auto Title Loans are Costly

Many people seek out auto title loans because they need money to take care of an emergency, pay off a bill, or to make a necessary purchase. These loans are attractive because they provide quick cash without depending on creditworthiness. However, these loans often cost far more than traditional loans or credit options. For an average loan of approximately $1.000, consumers will spend nearly $1.200 in fees. This is due to high interest rates on these loans and a variety of fees. These can include processing fees, origination fees, lien fees, late fees, and many other types of fees the company may add. For those with little income, additional loans may be necessary to pay off the original loan.

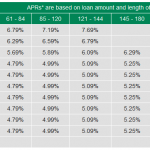

- High APR

The average auto title loan has an annual percentage rate or APR of 300%.. The annual percentage rate refers to the amount of interest charged in a year. On a $1000 loan, a year of interest would be equivalent to an additional $3000 added to the loan amount. However, most of these loans are short-term, so their interest amounts seem a lot lower. Unfortunately, most people who take out one of these loans renew them several times. In the end, they may pay that entire amount or more when fees are added. These costs are not beneficial to the borrower and often create a more difficult financial situation than they began with.

- Vehicles are Undervalued

The auto title loans are described as being based on the value of the vehicle being used as collateral. However, most auto title loans are only for 40-60% of the value of the vehicle. If the loan is not paid off, then the lender can take possession of your vehicle. The borrower is not getting a loan at the full value of the vehicle, but the lender can take possession of the vehicle for this undervalued loan amount. This means that the lender is going to make a profit off of the deal whether the loan is paid or not. They either profit from the very high interest rates and fees, or from the additional value from the vehicle above and beyond the cost of the loan.

- Leads to a Cycle of Debt

There are two types of auto title loans. One is where the loan is paid off with a single payment and one is paid off in multiple payments. Many people opt for the single payment option because the costs are slightly less than the multi-payment option. However, these loans can lead to a cycle of debt, especially those of the single payment variety. Because the costs are so high, many people that utilize these loans do not have enough money to pay back the loan in a single payment. This causes them to renew the loan. This renewal creates additional fees and interest costs. Only 12% of single-payment borrowers pay off the loan without renewal. One-third of these borrowers renew their loans more than seven times.

- Unclear Fees

Another major issue with auto title loans is that they are often unclear or vague about the fees they charge for the loan. Companies, such as TitleMax, only provide specific fee information if the borrower is a resident of Texas. To find out information about these fees, customers must call or visit a location to ask the representative about these fees. Unfortunately, these fees can often be obscure or confusing for borrowers. Many times, borrowers do not know or understand which fees and their costs will be charged until after they have received the loan.

- Losing the Vehicle

One of the biggest risks to getting an auto title loan is losing a vehicle. For many people, their vehicle is a necessary resource. It provides a means to get to and from work. If the vehicle is repossessed, borrowers are often unable to work and earn money to pay off the debt. Once the vehicle is repossessed, the lender will sell the car and keep any funds that come from the vehicle. IF that amount is less than what is owed, they can still pursue the borrower for the remaining funds. If the amount is over the value of the loan, often the lender will keep the additional money.

- Auto Title Loans are Poorly Regulated

Many states have banned auto title loans completely. However, there are many states that still allow these loans with very little regulation. Even with the regulations that are available, many of these companies find loopholes to avoid those regulations. In California, for example, there are limits to interest rates for small loans. This is why many lenders require that borrowers take out more than $2.500, regardless of their need. This lets the lender avoid the regulations on interest rates. In addition, some companies base their operations in other countries or Native American territories to avoid the regulations altogether.

- There are Many Scams

Auto title loans come with a lot of risks and unsavory practices that often leave people feeling as though they have been scammed. Unfortunately, most of these lenders are running a completely legal operation. However, there are many companies that disguise themselves as legitimate auto title lenders but, are in fact, scams. Some of these companies may be out to get information and access to bank accounts. Others actually provide loans, but have costs and fees completely hidden and can leave many borrowers unaware of the financial problems they are about to face.

- Federal and State Governments are Trying to Limit These Loans

Auto title loans prey on those who are in desperate need of extra money. They appeal to those who have little income and bad credit. Since most lenders do not provide credit to these borrowers, many borrowers have little other choice than to accept these types of loans. The federal and state governments have been looking into the practices of these lenders. Some regulations have been put into place; however, more regulation is needed. Hopefully, these regulations will be swift and help prevent the negative consequences of these types of loans.

It is important for any borrower to think seriously about entering into an agreement with these types of lenders. Although they may be more difficult for some to get financing, it is always best to look into alternative lending options before accepting these types of loans.

References

- https://www.titleloanser.com/stats/car-title-loan-statistics-trends-facts/

- http://www.statisticstats.com/finance/auto-title-loan-statistics/

- https://www.opploans.com/blog/steer-clear-title-loans-3-must-know-facts/

- https://www.nerdwallet.com/blog/loans/car-title-loans/

- https://www.finder.com/titlemax-auto-title-loans

- https://www.thebalance.com/car-title-loans-315534

- https://www.cheatsheet.com/money-career/5-shocking-facts-about-car-title-loans.html/

- https://www.creditkarma.com/auto/i/online-title-loans/

- https://www.carsdirect.com/auto-loans/be-aware-of-a-cash-loan-for-your-car-title-5-facts-for-avoiding-a-bad-loan

{kind=link}