Personal Loans

Sometimes you just need funds fast. Whether the need arises from a last-minute emergency or a long-term bucket list plan, traditional big bank lenders don’t cater to every borrower’s needs…and their application process often takes more time than you have.

If you are seeking a personal loan amount from $1,000 to $100,000 and need a quick application process to see if you qualify that won’t affect your credit, you have come to the right place.

You will find lenders with rates starting at 4.99% APR that can deliver a determination in just two minutes.

All you have to do is take these three easy steps:

1. Identify the loans you qualify for.

2. Choose a lender.

3. Complete that lender’s easy online application.

4. Execute the loan agreement and wait for your funds deposit.

It is that easy!

Why Consider a Personal Loan?

1. Consolidate your debt balances.

A personal loan can help you pull all your debt together and start paying it down at a much lower interest rate. Instead of juggling multiple payments from high interest lenders, get one easy monthly payment at an affordable interest rate.

2. Refinance your credit card debt.

Credit card debt is the most expensive kind of debt to carry, often assessing interest rates of 24% APR or higher on the unpaid balance. Credit card refinancing loans can get you out from under the ever-present burden of exorbitant interest rates and on the road to financial wellness again.

3. Finally make that major home improvement.

Home repairs are definitely more affordable than trying to sell and move to a new home. Yet just affording that much-needed home repair or home improvement project can itself present some financial challenges.

Most homeowners don’t have the means to do a remodel or major repair out of pocket. Get a home improvement loan with affordable interest rates and start working towards your dream home.

4. Find a loan even with bad credit.

Having bad credit can sometimes seem like a life sentence with no hope of parole. Paradoxically, taking out a loan can actually help improve your credit when you make timely repayments – but first you have to get a loan! Bad credit loans are available even for those who need to repair their credit.

Frequently asked questions about personal loans

What does “personal loan” mean?

A personal loan is simply borrowed funds for general use. Personal loans are often available from traditional lenders such as banks and credit unions. But increasingly, borrowers are turning to online lenders for faster, easier application processes and quicker access to borrowed funds.

Just as with traditional bank loans, you will have a monthly payment schedule that includes a portion of principle and interest.

How can you qualify for a personal loan?

Lenders are permitted to set their own application requirements, which is why it is smart to compare lenders before making your choice. In most cases, a borrower has to be at least 18, have U.S.A citizenship and a social security number, verify employment and income and have a certain credit score.

What amount can I get with a personal loan?

The amount varies depending on credit score, credit history and other factors, including how much debt you already have.

If I apply for a personal loan will it hurt my credit score?

Just checking to see what loans you qualify for will not hurt your credit score.

However, once you choose a lender and proceed to complete the formal application, this will trigger a credit check and may impact your credit score. The good news is that once you are approved for the loan and make prompt, timely repayments, this will then improve your credit score over time.

How fast will the funds arrive?

Different lenders have their own process, but in general expect the funds between same-day and one week.

What will my interest rate be?

For general purposes, shorter loan terms come with lower interest rates. If you elect to autopay using direct draft, you may also qualify for a lower interest rate.

Other factors that can impact the interest rate offered include credit history, credit score, current debt burden, type of personal loans and terms and the loan purpose.

What if I want to pay off my personal loan ahead of schedule?

This is permitted with most lenders but always check the fine print for something called a “prepayment penalty.” Some lenders will charge a penalty if you want to pay off your loan early because they receive less profits through interest repayments.

What can a personal loan be used for?

In most cases, a personal loan is considered a general purpose loan, which means the use of funds is up to you. You can use it for paying down personal debt or credit card debt, make major home repairs or renovations, purchase an emergency appliance or vehicle and similar other uses.

Always read the fine print of the lender’s loan terms carefully, since some lenders may specify what the funds can and cannot be used for. As well, in some cases the interest rate you are offered may fluctuate depending on the reason for seeking the loan.

What You Should Know When Applying for a Personal Loan

There are times in everyone’s life that there just isn’t enough money left at the end of the month. So then what happens if you hit a major expense, such as a car repair or your furnace goes out? An unsecured personal loan may be the answer you are looking for. These can also be helpful in situations where you are paying so much money each month on minimum payments that it will take thirty years to pay off your debt.

Traditional Loans vs. Personal Loans

The problem with a traditional loan is that the lender typically requires some type of collateral. Collateral is an asset that you offer to the bank that acts as insurance that you will pay the loan back according to their terms. When you need a loan to pay off debt or make a large purchase, you don’t have collateral. This is when an unsecured personal loan will be a good choice.

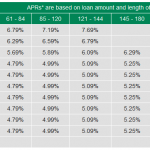

What’s the Interest Rate on a Personal Loan?

Interest rates and length of the repayment term will depend on several factors. Just like any extension of credit, your credit score and credit report will be reviewed. The lender will also assess your yearly income to determine that you have enough income to pay off the loan. If you have excellent credit, you can get great terms on a personal loan. Fair to poor credit scores will have a harder time securing a good deal, but you still may find a loan that is less interest than what you are currently paying. Interest rates may range from 13%-21% or more.

Do Your Homework

There are a few factors you should consider when shopping for a personal loan. These include:

- Interest rates. Don’t consolidate your loans if you will be paying more in interest.

- Payment amount. Be sure the minimum payment fits into your budget.

- Consider a co-signer. If your credit is poor, a co-signer can help you get better terms.

- Build your credit. If it’s not an emergency, consider waiting a few months to build your credit score in order to obtain better terms.

- Consider the financial implications. Consolidating all of your minimum payments into one lump sum can be a good idea if you can afford the payment. If it will strain your budget to the breaking point, however, there are other debt-relief programs that may be a better fit for you.

Compare Lenders Before Making Your Final Decision

If you decide that a personal loan is a viable option for your situation, you should compare several different lenders before deciding on one. Compare all of the terms, including whether there are any fees and what happens to the loan if you miss a payment. Knowledge is power in the financial world, so make sure you gain as much knowledge as you can before making your choice.