Asset-Based Loans with Real Estate Collateral

Utilizing both commercial and personal real estate to establish a business loan might appeal to some small business owners who have equity in their commercial property or home, and want to use the equity to acquire financing for their business. Numerous commercial properties are being put on the market every day, which is good news for business owners who want to control this real estate with a second or even a third lien in order to attain a credit line. According to a new report regarding commercial activity from the Commercial Buildings Energy Consumption Surveys, there are around 5,600,000 commercial properties in the U.S. as of 2012 – an increase of about 14% in the last ten years. As the number of commercial properties continues to increase (with some small businesses utilizing the space for owner-user properties), business owners can use the building’s or land’s net worth to get financing that conventional lenders wouldn’t normally provide them.

This article will discuss in more detail about how asset-based real estate loans work with real estate.

All About Asset-Based Lending

Asset-based lending, or ABL, is a practice that provides financing to a business that’s based on monetizing the balance sheet of the company. If the company’s assets include equipment and machinery, inventory, real estate or accounts receivables, these can be used to obtain financing as collateral. A line of credit is one of the most common forms of lending used to finance assets. Asset-based term loans are another form of lending people use. In addition to term loans and lines of credit, other asset-based lending forms include invoice financing, equipment leasing, factoring, and merchant cash advances. A lien (UCC-1) is placed on an asset once the asset-based lender funds the company.

Collateral and How It’s Used

Lenders use collateral to secure small business loans. After funding is given to the small business, the lender places a UCC-1 lien on the personal asset or business. If the borrower doesn’t pay the loan back, the lender seizes their collateral in order to recoup their losses. When the lender’s risk exposure is reduced, the borrower’s rates will be lower. Using collateral for secured business lending is a better option because the rates are much lower than non-secured business financing.

Types of Real Estate That Can Be Used as Collateral

In order to secure asset-based financing for a business, almost any commercial property can be used. Traditional lenders tend to place liens on commercial real estate when companies apply for term loans, but rarely use personal real estate to secure their financing. They do, however, make small business owners sign personal guarantees, which pledge all of their personal assets including personal real estate. On the other hand, asset-based lenders secure loans using the business owner’s personal land, property, or home. Lenders who use real estate to make asset-based loans realize that the borrower already has a mortgage so they will take second positions that are subordinate to the mortgage lender and will continue to provide financing for a 65 loan-to-value. This is certainly something to take into consideration.

Available Financing for Using Real Estate as Collateral

There are a variety of different financing options out there for companies that wish to unlock their real estate’s equity. From subprime asset-based lenders to top banks, there are many funding options including ACH financing, a line of credit, or a term loan. Bank lenders will use commercial real estate for term loans as collateral only. Other asset-based lenders will use the business’s cash flow and collateral to secure lines of credit. Subprime asset-based lenders structure financing similar to a cash advance service. This means they require weekly or daily repayments from the business’s bank account via ACH. Compared to traditional financing, rates tend to be much higher, but because real estate is being utilized to secure the loan, these types of asset-based loans have lower rates than cash advances which have higher interest rates.

Term and Rate Variations

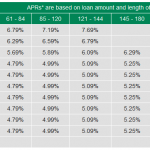

Depending on the quality and type of collateral that’s being pledged, the terms and rates of asset-based loans may vary. For instance, equipment and inventory have a loan-to-value of almost 50%, while accounts receivables have an LTV of 80%. Asset-based real estate loans in first, second, and third positions have up to a 65% LTV with varied rates. Asset-based loans offered by traditional lenders have single-digit rates, while subprime asset-based funding can have high interest rates up to around 20%. Terms start from as little as one year up to five years; however, the most common is between one and three years.

How to Secure an Asset-Based Loan

Depending upon which lender you choose, the process of obtaining an asset-based loan will vary. If you desire financing that’s traditionally asset-based, here’s is what you will need to have on hand:

Loan application

Schedule of liabilities

Collateral appraisals

3 years of balance sheets including those you have to date

A/P and A/R aging schedules

3 years of tax returns

3 years of income statements including those you have to date

If you choose to use personal land, real estate, commercial real estate, or another property for subprime asset-based lending, you will need to have the following:

Credit application

Collateral form

Bank statements

Title and BPO report

Once the lenders have received all of the required documents, the underwriting and due diligence process takes around one to four weeks to complete.

{kind=link}